Accounts & net worth

Four concepts, one idea: see all your money in one place.

- Account — a place where your money moves every day: the savings account, the credit card, cash.

- Asset — something valuable you own that doesn't move daily: stocks, crypto, your car, an apartment.

- Liability — a big debt: the mortgage, the car loan.

- Net worth — the full picture: everything you own minus everything you owe.

Accounts: your day-to-day money

You manage them under Profile → Accounts. There are four types: Checking, Savings, Credit card, and Cash.

When creating one you set a name, type, currency, starting balance (today's real balance — every transaction adds or subtracts on top of it, so your Finvot balance always matches the bank's), and optionally the bank. For credit cards you can also set the statement cutoff day.

Picking the bank isn't decorative

Linking your account to a bank helps Finvot recognize its alert emails, show its logo, and map Apple Pay payments to the right account.

The balance updates on its own with every transaction that arrives or that you log. If it ever doesn't match (transactions from before Finvot, say), edit the starting balance. And if you delete an account, its transactions are not deleted.

The number of accounts depends on your plan.

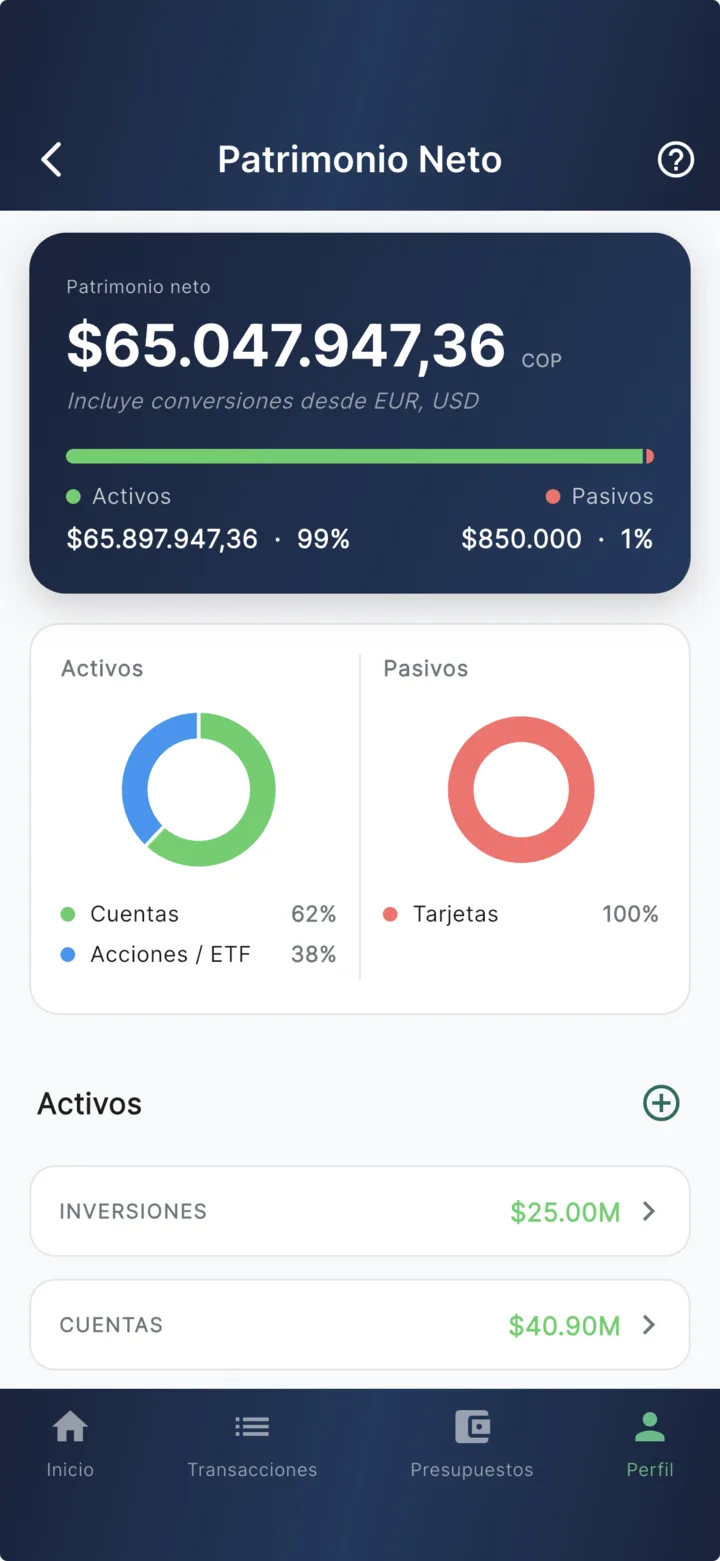

Net worth: the full picture

Profile → Net Worth is where the formula lives:

Part of the work is already done: your accounts flow in automatically. Savings, checking, and cash count as assets; credit cards (and any overdrawn account) count as liabilities. What's missing is what Finvot can't see — and that's what you add:

Assets: what you own

Tap + in the assets section and register investments (stocks, crypto, funds, pension, bonds), real estate, vehicles, or others. Each asset has a name, type, current value, and currency.

Since Finvot isn't connected to your broker or Binance, values update through manual valuations: every new value you record goes into the history, so you can see each asset's evolution over time.

Liabilities: what you owe

Just as simple: mortgage, car loan, student loan, or consumer credit, with today's outstanding balance and optionally the creditor. As you pay installments, update the balance with a new valuation.

The habit that makes it useful

Update the value of your investments and debts once a month. That turns net worth from a fun number into the metric that actually shows whether you're moving forward.

Good to know

- Multi-currency: everything converts to your primary currency using the most recent exchange rates from your transactions. If an asset can't be converted, Finvot tells you instead of making up a rate.

- Credit cards don't inflate your assets: their balance counts as debt, which is what it is.